Portfolio CECL PD Thresholds

A reproducible Bayesian monitoring approach that turns loan-level PD forecasts into auditable, portfolio-level thresholds.

Overview

Portfolio monitoring needs reliable PD thresholds, but simple mean +/- SD bands can be unstable and misleading for low-default portfolios. This project shows how loan-level PD outputs can be aggregated into portfolio-level alert bands that stay bounded, asymmetric, and easy to explain.

Approach

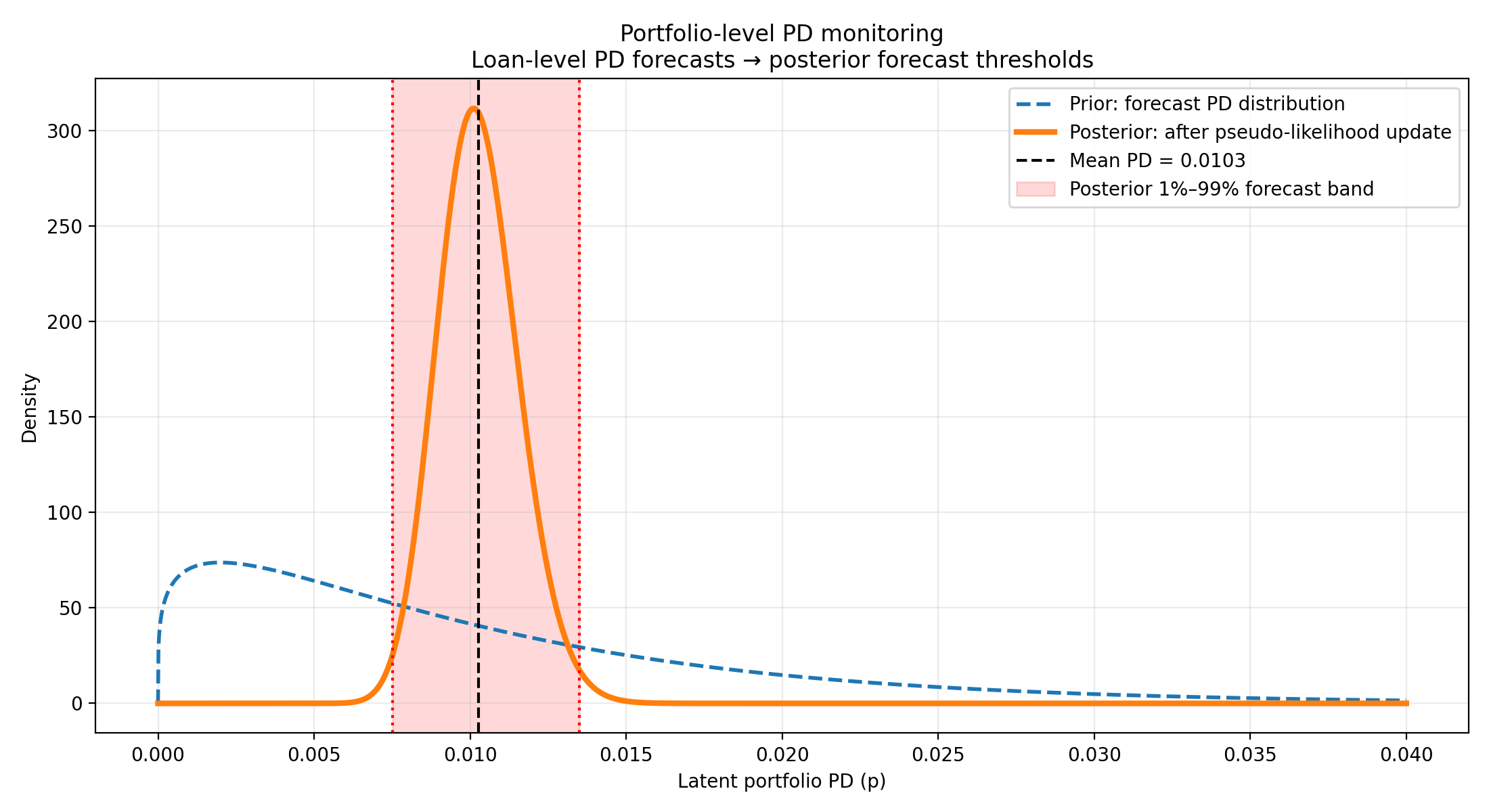

I fit a Beta prior to the forecast PD distribution and translate the forecast into an expected default count (N × mean PD), which is used in a conjugate update. The resulting posterior yields 1% and 99% percentiles that serve as forecast thresholds, providing a disciplined alternative to Gaussian bands.

Synthetic prior and posterior PD distributions showing how loan-level forecasts translate into bounded, asymmetric portfolio-level alert thresholds (1% / 99%).

Results

The posterior bands are tighter, bounded, and asymmetric, making them more actionable for portfolio monitoring, governance, and reporting. This approach generalizes across multiple portfolios (HELOC, CMM, SFR, and NOO CRE) without exposing any proprietary data.

Challenges

Proprietary data cannot be shared, so the method is explained using a transparent, synthetic-demo format. The pseudo-likelihood assumption needs clear documentation to remain auditable, while keeping the workflow reproducible for reviewers and model risk stakeholders.